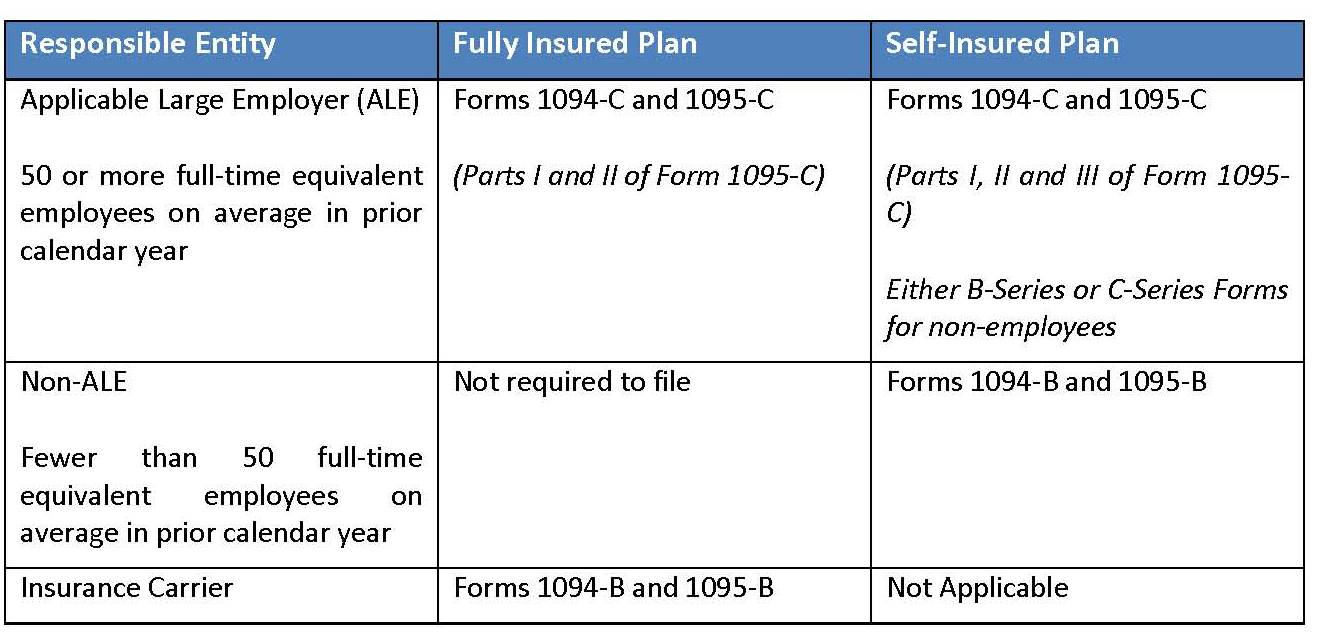

The Monday before the fourth of July, President Obama signed into law the Trade Preferences Extension Act of 2015, which contained several tax provisions in addition to the trade measures that were the focus of the bill. Among the tax provisions were changes that increase the penalties associated with failure to file or furnish correct “information returns and payee statements,” which include standard information returns, such as Forms W-2 and 1099, as well as the new reporting forms required by the Affordable Care Act (ACA). The following table summarizes the responsible parties and forms applicable to the ACA’s reporting requirements.

ACA reporting became mandatory for responsible entities starting in 2015. The first returns and statements will be provided in early 2016 reflecting the 2015 calendar year. Entities completing the employee statement (the 1095-B or 1095-C, as applicable) must provide one copy to employees and one to the IRS as part of the information return. Thus, a failure that relates to both the information return and employee statement may result in double penalties. For example, failure to send one copy of Form 1095-C to the employee and one copy to the IRS are considered two failures, which may trigger a $500 penalty. The IRS has stated that it does not intend to impose accuracy-related penalties on employers who complete the 2015 filings timely, as long as the employer was acting in good faith.

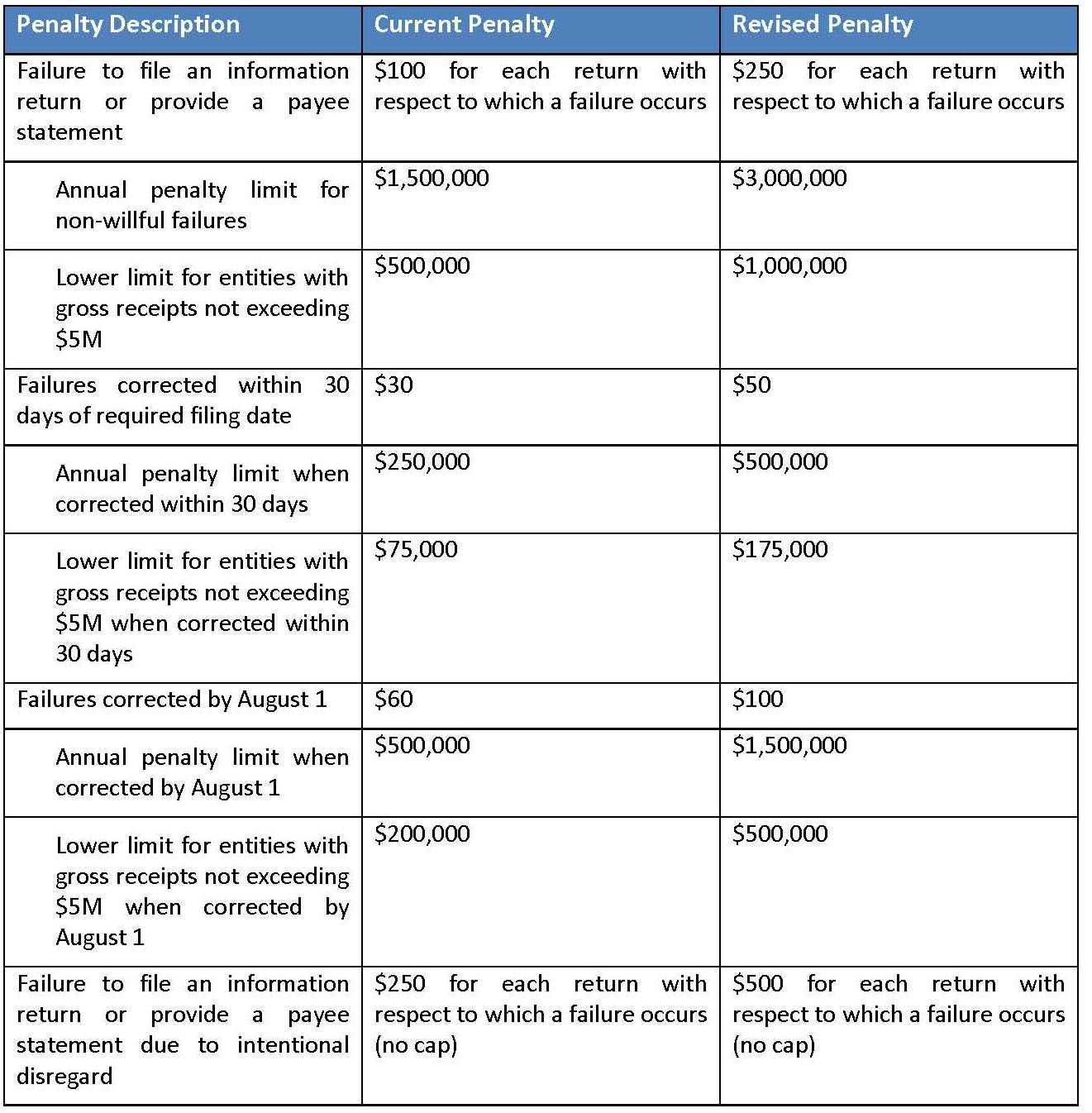

The table below reflects the current and revised penalty structure.

Filing Extensions

Filing Extensions

Employers should be able to obtain automatic extensions of time to file the ACA returns with the IRS; however, extensions of time to provide the employee statement (e.g., 1095-B or 1095-C) are more limited. It is our understanding that the IRS intends to revise form 8809—the existing extension form for W-2s and 1099s—to include the ACA forms as eligible for extension. Entities filing form 8809 before the returns are due are granted an automatic 30-day extension. An additional 30-day extension may be requested by submitting a second Form 8809 before the end of the first extension period. Requests for an additional extension of time to file information returns are not automatically granted. Generally, requests for additional time are granted only where it is shown that extenuating circumstances prevented filing by the date granted by the first request.

Extensions for Employee Statements Limited

Employers that require additional time to prepare the employee statements may request an extension of up to 30 days from the original due date (January 31) by submitting a letter to the IRS that contains certain information. There is not an automatic approval process for these types of extensions. The IRS is expected to release further information on the extension process for employee statements.

In the meantime, employers should work closely with their insurance broker and other trusted advisers when determining how their organization will address these new requirements.

Stacy Barrow advises UBF clients on various topics around ERISA and the ACA. One of the nation’s leading experts on the Affordable Care Act, Stacy uses a practical, business-focused approach to counsel his clients on all matters related to employee benefit plans. Stacy also has extensive technical knowledge and experience designing and implementing health and welfare plans that meet the numerous and intricate requirements of applicable federal and state law.